|

Epicor's

Mid-Market Pitch Becomes Higher

For (One) Scala

Part One: Event Summary

P.J.

Jakovljevic

- December 13, 2004

Event

Summary

While

the market has for some time

been buzzing about the (for

many still miraculous) predatory

comeback of SSA Global,

another true mid-market incumbent

vendor, Epicor Software

Corporation (NASDAQ:

EPIC), should be lauded too

for its recent revival. Like

SSA Global, and intriguingly

in the same time frame, Epicor

did not have much upbeat news

for several years following

on its progenitors’

(i.e., erstwhile Platinum

Corporation and Dataworks)

merger in 1998 and subsequent

name change from Platinum

to Epicor in 1999. Nevertheless,

in the past two years, Epicor

has seemingly achieved a turnaround

both in terms of its financial

performance and of its strategy

clarity. It has also for over

two years reverted to its,

this time possibly more selective,

acquisition streak starting

with the Clarus

e-procurement acquisition

at the end of 2002, and former

ROI Systems

and TDC Solutions

acquisitions mid-2003 (for

more information, see Epicor

Picks Clarus' Bargain At The

Software Flea Market

and Epicor

Conducts Its Own ROI Acquisition

Rationale).

As

highlighted in the above articles,

it appears this time though

that Epicor has learned some

hard lessons from its cumbersome

inception through mergers

that had initially resulted

in unrelated, diverse products,

and all in the face of the

overall weakness of the enterprise

resource planning (ERP)

market during 1999 and 2000.

Thus, the Scala

merger too seems to have much

of a strategic merit as opposed

to a knee-jerk, ‘me

too’ impulse owing to

the ongoing consolidation

craze in the market. While

customers want their enterprise

applications providers to

oblige them with new products

and technologies, vendors

in turn feel compelled to

increase revenues and market

share as to be able to justify

funding of new product development.

To

that end, Epicor

pledges to continue

to invest in its

products and to

grow both organically

and through acquisitions,

in order to assemble

the right mix

of back-office,

front-office,

and collaborative

e-business functions,

delivered under

a single-point

accountability

(i.e., “one-stop

shop” and

“one throat

to choke”)

approach that

is overwhelmingly

desired by its

target market.

While in the past

Epicor would integrate

with partner products

for best-of-breed

solutions to accommodate

these requirements,

it has lately

been expanding

the boundaries

of traditional

ERP by building

fully integrated

applications that

are based on the

same technology

and toolsets,

and possibly delivered

all from a single

vendor.

Epicor

Acquires Scala

Accordingly,

back at the end

of 2003, Epicor

and Scala

Business Solutions

(Euronext: A.SCALA),

an Amsterdam,

the Netherlands-based

provider of collaborative

enterprise software

for mid-size enterprises

and subsidiaries

of global corporations,

jointly announced

that the expectation

was justified

that they would

reach agreement

on a merger. The

proposed merger

was effected by

a public offer

by Epicor for

all the outstanding

ordinary shares

in the capital

of Scala at an

anticipated aggregate

transaction value

of approximately

$87 million (USD)—the

equivalent of

Euro3.27 per ordinary

share—,

as of the closing

price on November

13, 2003, consisting

of a cash price

of $ 41.7 million

(USD) subject

to adjustment,

plus 4.1 million

shares of Epicor’s

common stock.

The offer was

made up of a cash

price of $1.823

(USD) per Scala

share plus 0.1795

shares of Epicor’s

common stock.

The

public offer only

commenced following

the completion

of Epicor’s

due diligence

investigation

of Scala, the

receipt of a fairness

opinion by Scala,

regulatory approvals,

the filing of

an S-4 registration

with the Security

and Exchange Commission

(SEC) by Epicor,

and other customary

conditions including,

among others,

material adverse

changes to Scala

and management

retention agreements.

Initially, Epicor

anticipated that

it would begin

the public offer

for all outstanding

ordinary shares

of Scala and publish

an offer memorandum

in December 2003,

and close the

transaction in

the first quarter

of 2004. The combination

was then also

expected to be

accretive to Epicor’s

Generally Accepted

Accounting Practice

(GAAP) earnings

in the second

quarter of 2004

and for the fiscal

year 2004.

One

of the requirements

for delisting

Scala’s

stock on the Dutch

exchange was that

at least 95 percent

of the ordinary

shares of Scala

are offered. As

said earlier,

the anticipated

transaction value

of approximately

$87 million (USD)

was to be paid

partly in cash

and partly in

Epicor common

stock, with a

20 percent downwards

protection for

the shareholders

of Scala. Any

decrease in the

value of the common

stock of Epicor

below a floor

of $10.21 (USD)

per share was

to be compensated

in cash by an

adjustment in

the offer price.

The anticipated

transaction price

of approximately

$87 million (USD)

represented a

premium of approximately

40 percent as

of the closing

price of Scala’s

shares on November

13, 2003, and

a 59 percent premium

on the basis of

the 30-day share

price average.

The closing of

the transaction,

which was expected

to occur in early

2004, was subject

to certain conditions

including, but

not limited to,

regulatory clearance

and acceptance

by Scala shareholders,

whereas the Dutch

regulator of the

financial markets

(Netherlands Authority

for the Financial

Markets) and Euronext

had been informed

of the intended

bid. SG

Cowen Securities

Corporation was

adviser to Epicor

and Fortis

Bank Corporate

& Investment

Banking

was adviser to

Scala, with respect

to the transaction.

However,

the acquisition

closing process

was delayed for

one major reason,

which was the

ensued restatement

of Scala’s

US GAAP financial

figures by its

auditor KPMG,

so that it was

not until mid-June

that Epicor was

able to declare

its public offer

to acquire all

issued and outstanding

ordinary shares

in Scala unconditional.

As of the tender

closing date,

approximately

21.7 million Scala

shares have been

tendered into

the offer, and

upon the delivery

of these Scala

shares, Epicor

was to hold approximately

93.2 percent of

the issued share

capital of Scala.

Epicor then conducted

a subsequent tender

period for holders

of Scala shares

who had not yet

tendered their

shares, which

expired effective

July 5. Following

the completion

of that subsequent

tender period

and the tendering

of 1,096,048 shares

in the period,

corresponding

with approximately

4.54 percent of

all outstanding

Scala shares,

Epicor now holds

a total of approximately

97.98 percent

of all outstanding

Scala shares.

Consequently,

Euronext Amsterdam

N.V. then confirmed

that the listing

of the Scala shares

on the official

market of Euronext

Amsterdam N.V.

would terminate

as of July 13,

2004, whereby

July 12, 2004

was the last trading

day of the Scala

shares on the

Euronext exchange.

What

the Merger Creates

The

merger by all

accounts creates

the largest independent

global mid-market

provider of collaborative

ERP, customer

relationship management

(CRM), and supply

chain management

(SCM) applications

based on Microsoft’s

.NET

platform and Web

services, with

approximately

$250 million (USD)

annual revenue

run rate, nearly

1,500 employees,

and with over

20,000 customers.

The combined company

hopes to expand

its global presence

with worldwide

coverage of sales,

consulting, and

support for mid-market

and large multinationals

as well as local

enterprises, offering

a broad suite

of integrated

solutions.

Both

Epicor and Scala

customers should

now be served

by a global entity

with the reach

and scale to more

effectively support

their operations,

and will be well

positioned for

growth with local

support in emerging

markets, and in

key markets where

Scala traditionally

performs well,

such as Scandinavia,

Russia, Central

and Eastern Europe,

and China. Scala’s

customer base

is predominantly

European , while

Epicor’s

largest customer

base predominantly

in North America,

Australia, and

the UK. The resulting

company’s

revenues will

therefore be diversified

across regions

with approximately

52 percent of

its revenue base

in North America

and 48 percent

outside this region.

The

combined company

plans to further

support and develop

iScala

products, while

Scala’s

management was

offered one board

seat out of six

on Epicor’s

board of directors.

In the long term,

the combined company’s

product offering

would be developed

using the functional

synergies of all

products, and

the integration

advantages of

the .NET framework

and Web services.

Enlarged Epicor

pledges to continue

the unwavering

commitment to

developing and

bringing to market

software and services

based on Microsoft

technology, given

its strong Microsoft

partnership—as

a globally managed

independent

software vendor

(ISV) and Microsoft

Global ERP Ecosystem

partners—and

has actively participated

for many years

in numerous Microsoft

joint development

programs and early

adopter technology

initiatives.

The

merger may also

bode well for

Epicor’s

expanded presence

in key growing

verticals including

financial services,

consumer packaged

goods (CPG),

professional services,

automotive, industrial

machinery, light

engineering, electronics,

hospitality, pharmaceuticals,

and nonprofit.

Also, this might

increase the vendor’s

scale and reach

to support global

multinational

corporations with

a worldwide infrastructure

for sales, consulting,

and support, and

a strong partner

channel—combining

over 400 partners

worldwide, with

possible operating

and infrastructure

synergies in general

and administrative

(G&A), research

and development

(R&D), facilities,

and technical

support with a

solid platform

and infrastructure

for future strategic

and tactical acquisitions

in a consolidating

market.

Prior

to the merger,

Epicor had delivered

its solutions

to over 15,000

customers worldwide,

whereby its manufacturing

customer community

includes over

6,500 customers,

implemented in

more than thirty-five

countries. Epicor's

broadening suite

of integrated

software solutions

features CRM,

financials, manufacturing,

SCM, professional

services automation

(PSA), and collaborative

commerce applications.

On

the other hand,

Scala’s

main trump is

unrivaled localization

capabilities for

companies doing

business in established

or emerging markets,

or even in some

of the world’s

most difficult-to-get-to

places. Scala

has garnered the

local know-how

and expertise

to deliver results

for businesses

almost anywhere

in the world,

from over twenty-five

years working

with international

companies and

their subsidiaries

and divisions

in many types

of industries.

Scala delivers

software and services

that support local

currencies, accounting

regulations, and

legal requirements

in more than thirty

languages in over

140 countries.

Epicor

Financials

Since

the transaction

closing, Epicor

has reported two

quarters of earnings,

most recently

the October 20

upbeat announcement

of financial results

for the third

quarter ended

September 30,

2004. For a protractedly

languishing company

until not that

long ago (see

figure 1), reporting

facts like that

the Q3 2004 revenues

grew over 54 percent,

year-over-year,

whereby Q3 2004

license revenues

grew over 64 percent,

year-over-year,

second quarter

GAAP earning

per share

(EPS) grew over

whopping 175 percent,

year-over year,

while the vendor

added over 165

new customers

to its base and

it released over

50 product upgrades

to market across

its suite of solutions,

and so on, should

bear a great importance

and vindication

to the long-embattled

but persistent

management.

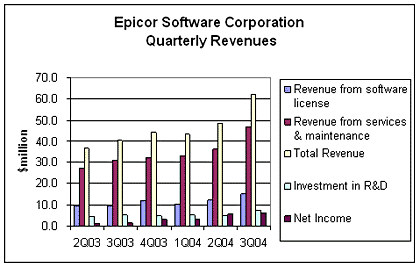

Figure

1

Total

revenues for the

quarter were $62.2

million (USD),

up over 54 percent

compared to $40.3

million (USD)

for Q3 2003, whereby

it included $17.5

million (USD)

in total revenues

from Epicor’s

recently acquired

subsidiary Scala

Business Solutions

N.V., whose revenues

have fully contributed

for the first

time to this quarterly

report. Excluding

the contribution

from Scala, Epicor’s

total revenues

grew 11 percent

year-over-year.

Software license

revenue totaled

$15.3 million

(USD), a 64 percent

increase compared

to $9.4 million

(USD) a year ago

and including

$4.7 million (USD)

for the contribution

from Scala (see

figure 2). Excluding

the contribution

from Scala, Epicor’s

license revenues

grew approximately

13 percent year-over-year.

Figure

2

Consulting

and maintenance

revenues for the

third quarter

were $45.9 million

(USD) compared

with $30.4 million

(USD) in the third

quarter of 2003,

up over 50 percent.

Included in consulting

and maintenance

revenues was $12.6

million (USD)

from Scala’s

contribution.

Excluding the

contribution from

Scala, Epicor’s

consulting and

maintenance revenues

grew approximately

10 percent year-over-year.

GAAP net income

for the third

quarter was $6.3

million (USD),

which compares

with net income

of $1.8 million

(USD) in the prior

year’s period.

For the quarter,

adjusted earnings

were $9.6 million

(USD) compared

with adjusted

earnings of $4.7

million (USD)

in the same period

last year. Adjusted

earnings exclude

amortization of

capitalized software

development costs

and acquired intangible

assets, stock-based

compensation expense

and restructuring

charges, and other.

Further,

Epicor ended the

quarter with cash

and cash equivalents

of $46.6 million

(USD), up approximately

2 percent from

the prior quarter,

including significant

cash expenditure

for transaction

costs, Sarbanes-Oxley

costs, and severance

costs following

the reduction

in force completed

during the quarter

as a result of

consolidating

the Epicor and

Scala organizations.

For

the fourth quarter

2004, the company

raised its previously

issued total revenues

expectations from

the range of $66

to $67 million

to $67 million

(USD) in total

revenues, while

for fiscal year

2004, the company

raised its previously

issued total revenue

guidance of $220

million to $221

million (USD).

Additionally,

the company provided

an initial outlook

for fiscal year

2005, where it

anticipates the

revenues to be

approximately

$273 million (USD)

The company has

also completed

extensive operational

reviews of its

Scala acquisition

and put in place

plans toward achieving

its cost synergies

and accretion

goals, which was

demonstrated in

the last quarter.

How

Scala Complements

Epicor

Epicor

Software Corporation

(NASDAQ: EPIC)

and Scala

Business Solutions

(formerly Euronext:

A.SCALA, delisted

in July 2004),

an Amsterdam,

the Netherlands-based

provider of collaborative

enterprise software

for mid-size enterprises

and subsidiaries

of global corporations

have completed

a merger that

began in late

2003. The merger

creates the largest

independent global

mid-market provider

of collaborative

ERP, customer

relationship management

(CRM), and supply

chain management

(SCM) applications

based on Microsoft’s

.NET

platform and Web

services, with

approximately

$250 million (USD)

annual revenues,

nearly 1,500 employees

and with over

20,000 customers.

The combined company

has an expanded

global presence

with operations

and customers

in 143 countries,

including worldwide

coverage of sales,

consulting and

support for mid-market

and large multinationals

as well as local

enterprises, offering

a broad suite

of integrated

solutions.

Given

Epicor’s

ordeal of the

past and the fact

that divesting

two lateral products

in 2001 greatly

helped it achieve

some much needed

stability nowadays

(see Latest

Development on

Epicor's Trying

The Divestiture

Tack),

one could wonder

about the wisdom

of the renewed

Epicor’s

appetite for acquisitions.

After all, the

acquisition of

former Dataworks

had left Platinum

(subsequently

Epicor) with multiple

unrelated ERP

products and the

inherited daunting

task of rationalizing

its product development

strategy, and,

who on earth with

a sound mind would

like to revisit

that experience?

Well, concurrently

with achieving

a turnaround both

in terms of its

financial performance

and of its strategy

clarity, Epicor

has also for over

two years reverted

to its, this time

possibly more

selective, and

thus successful

acquisition streak

starting with

the Clarus

e-procurement

acquisition at

the end of 2002,

and former ROI

Systems

and TDC

Solutions

acquisitions mid-2003

(for more information,

see Epicor

Picks Clarus'

Bargain At The

Software Flea

Market

and Epicor

Conducts Its Own

ROI Acquisition

Rationale).

Moreover,

one should note

that Epicor has

since its progenitor’s

inception twenty

years ago been

competing primarily

in the true mid-market,

which it defines

as enterprises

with revenues

between $50 million

and up to $1 billion

(USD), and to

that end, the

vendor has competed

mainly with the

Vantage

(for new business

opportunities),

Manage

2000,

and Avant�

products in the

manufacturing

arena, and with

the Epicor

Enterprise

suite (formerly

e by Epicor)

and the Clientele

standalone CRM

product for certain

service industries.

Increasingly,

since customers

in this mid-market

segment are looking

for Microsoft

SQL Server-based

solutions, the

Vantage manufacturing

product (and its

“smaller

sibling”

Vista,

as an introductory-level

product) have

turned out as

better positioned

to address this

requirement, although

both major manufacturing

product lines

include the broad

range of modules

for the upper

echelon of midsize

manufacturing

enterprises.

Scala

Products

Therefore,

Scala should complement

and further bolster

Epicor’s

offering in many

regards, but possibly

the royal one

would be its ability

to firmly position

Epicor as a standardized

tier 2 or divisional

solution for Global

1000 companies.

This is owing

to Scala’s

unrivaled global

product capabilities

amongst peer vendors,

which will be

explained in more

detail later in

the text. Otherwise,

at first glance

the merger looks

like a positive

move for both

companies and

their customers,

since Epicor obtains

a foothold in

some complementary

geographic regions,

and in certain

discrete manufacturing

and service industries

where it has not

really penetrated

in the past (e.g.,

industrial machining,

pharmaceuticals,

light engineering,

hospitality, retail,

not-for-profit

[NFP] organizations,

etc.) by acquiring

a reasonably run

vendor without

much excessive

baggage.

It

is interesting

to note that during

Epicor’s

trying years at

the turn of the

century Scala

had performed

much better. For

example, although

the market turbulence

during these few

years had also

taken its toll

in Scala’s

restructuring

and cost-containment

exercise, still,

with revenue of

approximately

EUR 74 million

in 2002, which

was a slight 4

percent growth

over 2001, Scala

then remained

a prominent mid-market

enterprise applications

provider. Although

its license revenue

declined by 7

percent in 2002,

the maintenance

revenue increased

by 23 percent,

given that more

than 90 percent

of existing customers

continued to pay

for maintenance.

This was, in part,

due to an aggressive

development program,

which saw the

release of iScala

2.1 in

mid-2002 (see

Scala

Shows Far More

Than a Bit of

a Backbone)

and a newer version

iScala

2.2 in

2003. From 2001

to the end of

2002, the company

also doubled its

research and development

(R&D) headcount

to over 200 (out

of a 700 total

employee headcount

at the time),

plus 50 development

contractors, and

geared up its

in-house training

center, the Scala

University

in Budapest, Hungary

to train and certify

its growing ranks

of 140 resellers

that accounted

for 23 percent

of its business

in 2002.

But,

despite impressive

growth and cash

flow during these

years, Scala unfortunately

posted a quite

disappointing

performance in

early 2003, possibly

at an unwanted

time, resulting

with a restructuring

program that included

rationalization

of the company’s

bloated R&D

base with the

closure of some

satellite R&D

facilities and

the transfer of

expertise to the

company’s

cost-effective

center of technical

R&D excellence

in Moscow, Russia,

and headcount

reduction of approximately

30 percent from

the previous employee

level, including

consolidation

of a number of

senior management

positions.

Possibly

more disconcerting

was the fact that

long-standing

customer interest

in the new functionality

of Web services-enabled

iScala 2.2 release

then resulted

in overcommitment

to customer-related

developments (whereas

the iScala 2.1

release was mainly

focused on improvements

in the underlying

technology platform).

As a result, the

commercial release

had to be delayed

to September 2003

instead of previously

indicated mid-2003.

This delay created

a vicious circle-like

adverse impact

on new license

sales, as customers

had to wait for

new functionality.

Even as all these

events took place

at possibly the

worst time for

Scala,,Epicor,

who struggled

at the turn of

the century, had

ironically meanwhile

quite straightened

its ship to even

appear attractive

as a savior to

former Scala board

in 2003.

Also,

these rationalization

measures and the

eventual release

of the product

have reverted

to increased revenues

and a positive

operating income

afterwards. Namely,

by the end of

2003, Scala’s

results were again

exceeding expectations

owing to a new

product released

in September,

iScala

2.2 Collaborative

ERP,

which was hailed

as the biggest

release of new

functionality

in more than 10

years, and which

has several modular

or individual

enhancements of

interest to manufacturers,

including service

management, CRM,

SCM, asset management,

contract management,

resource management,

business intelligence

(BI), workflow

management, user

interface

(UI) customization,

and connectivity.

The

company has since

reportedly seen

strong customer

demand for the

new iScala version,

reflected in its

healthy sales

pipeline, especially

in markets where

Scala traditionally

performs well,

including Scandinavia,

Eastern Europe,

Russia, and China.

Nearly 60 percent

of Scala’s

top customers,

including both

global and local

enterprises, have

supposedly been

actively involved

as early adopters

since 2002, with

many of them already

running the new

version live.

As an example,

Tetra

Pak is

one of Scala’s

longest-standing

customers, with

Scala solutions

implemented in

nearly fifty countries,

against SAP

at the corporate

level.

iScala

2.2

The

iScala 2.2 Collaborative

ERP system includes

- iScala

Core Business

Processes,

which is a set

of business

processes that

includes multicurrency

and multi-legislative

financial functionality,

asset management,

and a set of

packaged integration

solutions (eXtensible

markup language

[XML]-electronic

data interchange

[EDI], financials,

and master data

integration)

which helps

customers to

improve the

business efficiency

of their core

processes.

-

iScala

CRM,

which is powered

by Microsoft

CRM

(for more information,

see Scala

and Microsoft

Become (Not

So) Strange

CRM Bedfellows),

accessible from

both Microsoft

Outlook and

the Web, and

integrates with

iScala ERP and

other business

systems.

-

iScala

SCM,

which is packaged

to address typical

business needs,

starting with

logistics (purchase

and inventory

management),

warehouse management

(including quality

control), manufacturing

(planning, configuration,

shop floor control),

tools (such

as lead time

management,

available

to promise

[ATP] and drop

shipment), and

integration

solutions.

-

iScala

Contract Management,

Project

Management,

Service

Management,

which is a set

of business

processes that

has been significantly

improved and

extended in

the new version

of iScala to

help customers

automate their

pertinent business

processes.

-

iScala Human

Resource Management,

which includes

the global version

of the iScala

Payroll

module that

customers can

use to improve

their personnel

management in

almost any country,

regardless of

how complex

the legislation

requirements.

-

iScala Business

Intelligence

(BI) Server,

which provides

a broad set

of BI and analytics

tools to give

users access

to information

they need when

they need it

to make the

right decisions

quickly. Designed

to make operational

and management

reporting easier,

the product

enables users

to relatively

quickly perform

drill-down enquiries

and comparative

analysis to

find out exactly

how the business

is doing and

where improvements

are needed.

-

iScala

Developer,

which is an

entire development

solution for

creating vertical

and unique company-specific

processes inside

and outside

the iScala system.

Thereafter,

in May, Scala

announced that

the first service

release (SR1)

of the latest

version of the

iScala Collaborative

ERP system is

now available

for all existing

and potential

customers worldwide.

iScala

2.2 SR1

includes a wide

range of new and

enhanced business

functionality,

such as better

connectivity with

other best-of-breed

warehouse and

manufacturing

systems, improved

features in the

supply chain and

service management

processes as well

as availability

in two additional

languages—Korean

and traditional

Chinese.

The

company has also

enhanced its iScala

CRM offering to

give customers

better visibility

into the sales

pipeline and across

sales activities,

to improve the

quality of leads

and closure rates

and be able to

fully integrate

with Microsoft

Outlook and other

Microsoft

Office

programs. iScala

CRM now comes

with standard

reports that are

reasonably fast

and easy to run

and with a familiar

interface, similar

to Outlook,

which will possibly

help a company

extend its applications

to more users.

For example, a

user can create

a sales proposal

from a Microsoft

Word template,

use pricing data

from their iScala

ERP system, and

save all versions

of that proposal

within iScala

CRM, keeping track

of all the changes

in the sales cycle

until the sale

is closed.

Last

but not least,

the addition of

a brand new iScala

Manager Software

Developer Kit

should interest

Scala’s

indirect channel,

who will now be

able to add further

value by designing

new business processes

that can easily

be added to the

standard iScala

workflow, to support

customer- or industry-specific

needs.

Market

Impact

Epicor

Software Corporation

(NASDAQ: EPIC)

and Scala

Business Solutions

(formerly Euronext:

A.SCALA), an Amsterdam,

the Netherlands-based

provider of collaborative

enterprise software

for mid-size enterprises

and subsidiaries

of global corporations,

have completed

a merger that

began in late

2003. The merger

creates the largest

independent global

mid-market provider

of collaborative

ERP, customer

relationship management

(CRM) and supply

chain management

(SCM) applications

based on Microsoft’s

.NET

platform and Web

services, with

approximately

$250 million (USD)

annual revenues,

nearly 1,500 employees,

and with over

20,000 customers.

The combined company

hopes to expand

its global presence

with worldwide

coverage of sales,

consulting, and

support for mid-market

and large multinationals

as well as local

enterprises, offering

a broad suite

of integrated

solutions.

Thus,

Scala, with main

direct office

coverage in Europe

and the Far East,

and through its

network of partners

and dealers in

most remote, esoteric,

and still low-penetrated

markets, perfectly

fits the description

of an ideal Epicor

supplement. Another

factor that may

bode well for

its future as

Epicor’s

subsidiary is

its vast international

coverage, and

a broad geographic

revenue mix (over

4,500 customers

with over 7,500

sites worldwide),

which not many

(if any) peer

vendors can tout.

Scala has offices

in over thirty

countries, with

local distributors

increasingly helping

out the direct

sales force, whereas

the vendor has

continued to offer

its products and

services through

the reseller channel

and value

added resellers

(VAR), which has

also expanded

lately, with 54

percent license

revenue growth

in 2002 and with

a 34 percent growth

in number of partners

amounting to over

140 partners worldwide.

The

above facts have

long promoted

Scala into a serious

challenger in

the mid-market,

especially in

emerging markets

like Central and

Eastern Europe,

Middle East, and

China (possibly

the local market

leader therein

following up on

the early entry

in the 1980s).

The former flagship

Scala

5.1,

a mature but less

technically apt

ERP product suite,

has traditionally

covered the full

spread of core

ERP modules, including

logistics, manufacturing,

financials, project

management, and

service management,

with the indication

of high levels

of customer satisfaction.

Like SYSPRO,

its parent-to-be

Epicor, Intuitive

Manufacturing

Systems,

and Exact

Software,

Scala’s

functionality

is equitably solid

in accounting,

manufacturing,

and material management

areas. This is

an advantage compared

to competitive

products that

are either mainly

strong in accounting

(e.g., Microsoft

Business Solutions

[MBS],

Sage/Best/ACCPAC,

Coda,

Systems

Union/SunSystems,

Unit 4

Agresso,

etc.) or in manufacturing

or distribution

(e.g., Lilly

Software,

SoftBrands,

Made2Manage,

or QAD).

Scala

Market Strategy

At

the beginning

of 2000, Scala

began redesigning

its ERP software

and building a

new platform specifically

for on-line collaboration.

It has meanwhile

packaged together

the functionality

required in one

standard software

system, which

means a business

can begin collaboration

with its subsidiaries,

customers, partners,

and suppliers.

To that end, iScala

2.1 was

the successor

product to Scala

5.1, since it

contained all

of the basic ERP

functionality

that was available

in Scala 5.1 in

addition to the

collaborative

capabilities inherent

to the new XML

Web services-based

design. Scala

5.1 was withdrawn

from new business

sales in December

2002, although

existing customers

will continue

to receive support

well into the

future.

Like

its predecessor,

iScala

2.2 also

comes in two flavors

to satisfy needs

of both local

medium business

and of smaller

global corporations

(and their subsidiaries,

divisions, and

suppliers). The

iScala

Business Server

is an entry-level

product—a

collaborative

ERP package for

the medium-size

stand-alone business

needing core ERP

functionality

without a need

for high scalability

and advanced security,

and as a first

step towards automating

business processes

across applications

and with customers

or suppliers systems.

iScala Enterprise

Server,

on the other hand,

is designed as

a more complete

collaborative

ERP package for

medium-size multinational

companies or for

the subsidiaries

and divisions

of larger enterprises.

It has all the

functionality

of the iScala

Business Server

but adds scalability,

business centralization

capabilities,

and support for

working across

and supporting

multiple sites

and subsidiaries.

Thus,

Scala prefers

not to be simply

perceived as a

mid-market vendor

per se, as it

rather targets

two somewhat distinct

mid-market segments:

1) mid-size units,divisions,

or subsidiaries

of large corporations,

and

2)

independent mid-sized

enterprises, where

Epicor’s

sweet spot has

also primarily

been so far. There

are slight variations

in the needs of

these two mid-market

types, since the

corporate divisions

typically have

urgent connectivity

needs such as

processing multinational

invoices, using

integrated warehouse

systems, or triggering

automatic purchase

and sales orders.

Unique

Multilingual Capabilities

Accordingly,

Scala has long

featured possibly

the unique multilingual

capabilities of

its Collaborative

ERP software.

Scala maintains

a single set of

application code

for all its languages—more

than thirty—compared

to other vendors

who commonly support

different software

versions for different

languages. Scala’s

product architecture,

which enables

a single version

of the software

to support multiple

languages, means

global companies

can keep their

maintenance costs

down by, for example,

running a single

service center

to support several

countries. It

also gives them

flexibility to

manage their global

business more

easily in a multilingual

and multicultural

environment, since

Scala also provides

telephone support

in over fifteen

different languages

to support local

users worldwide.

To

ensure that every

new product is

multilingual from

the start of its

life cycle, translation

into different

languages is done

in the software

development process

on a phrase-by-phrase

basis to give

accurate meaning

in multiple languages.

The multilingual

capabilities are

enhanced by the

new Unicode technology

that is used starting

with iScala 2.1,

allowing the combination

of any languages

with different

characters in

a single installation.

True multilingual

technology like

Unicode also allows

a wide range of

languages such

as Chinese, Russian,

or Arabic, to

be stored, displayed,

and printed on

the same page

or even in the

same field. The

technology also

gives Scala a

significant technical

advantage in that

new developments

and maintenance

updates to Scala

software only

have to be developed

in a single version,

whereas Scala’s

competitors typically

have to maintain

multiple versions,

one for each language.

Consequently,

having long focused

on the upper end

of the ERP mid-market,

Scala has apparently

demonstrated an

understanding

of this market’s

dynamics and its

pragmatic requirements

of robust multinational

corporate functionality

and intra-enterprise

visibility within

a fairly inexpensive

product, fast

and simple implementations,

and reliable service

and support. The

company has struck

the value proposition

of balancing business

processes standardization

with flexibility

and autonomy of

remote subsidiaries,

which should come

in handy for Epicor’s

like forays.

Global

companies should

appreciate iScala’s

features such

as simultaneous

support for multiple

accounting standards,

enhanced security

and usability

features, and

remote administration

tools to manage

distributed or

local installation,

which can often

match or exceed

the tier one vendors’

capabilities.

Many other peer

vendors conversely

require their

customers to operate

in a single language

at each location

because their

applications are

based on the technology

unable to hold

more than one

language in the

same system.

With

recently increased

business functionality,

comprehensive

integration, and

connectivity capabilities

coupled with a

brand new flashy

UI, iScala 2.2

might be an attractive

choice for companies

who are considering

upgrading or buying

a new ERP system.

There might be

no similar product

that provides

companies with

consistent information,

a global view

of the business,

one view of customers

or suppliers,

and reasonably

rapid system deployment

at the same time.

While

tier one enterprise

systems can cope

with the complex

needs of centralized

functions and

a large number

of users, they

are often not

well-suited to

handling the less

complex needs

or localization

requirements of

a branch or sales

office in remote

countries. Hence,

Scala (and now

Epicor too) wants

to cohabit with

these global players

by providing systems

for subsidiaries

and regional offices

of global enterprises.

Scala’s

argument would

be that it is

simply too expensive

and time consuming

to keep changing

a rigid tier one

product to suit

a changing market,

even if it could

be deployed in

a location where

often the poor

telecommunications

infrastructure

capability would

prevent a web-deployed

system from being

used.

Vertical

Specialization

Scala’s

endeavor at some

vertical specialization,

operating with

a wide range of

specialist channel

partners around

the world, many

of whom target

specific application

areas, such as

the pharmaceuticals

business (over

500 sites) and

the hospitality

industry (over

300 customers),

is also commendable,

although these

are perceived

and marketed as

stand-alone solutions,

separate from

iScala. Thus,

these solutions

will have to inevitably

migrate to the

new iScala platform

in a foreseeable

future. Also,

a number of Scala

customers work

in discrete engineer-to-order

(ETO) and make-to-order

(MTO) manufacturing,

and require full

project based

accounting capabilities.

Because one of

the main businesses

of these global

companies is to

manufacture in

lower cost geographic

locations, the

vendor has made

attempts to ensure

that iScala's

capabilities at

least match the

demands of the

medium to small

manufacturing

subsidiary, whether

it be for ‘to

stock’ or

‘to order’

manufacturing

environment.

Still,

independent Scala

had yet to build

or acquire many

aspects of the

extended-ERP functionality,

especially supply

chain planning

and execution

(SCP&E) and

product lifecycle

management

(PLM) functional

enhancements to

round out a complete

collaborative

extended-ERP suite,

readily available

by many of its

peers let alone

the tier one likes

of SAP,

SSA Global,

PeopleSoft,

Oracle,

Intentia,

and IFS.

Not to mention

the need to bolster

strategic supplier

relationship management

(SRM) and sourcing,

manufacturing

operational capabilities,

and shop floor

execution, well

beyond a mere

order management.

Some of iScala’s

clever features,

like Global ID

(a unique identifier

to be assigned

in all of client’s

enterprises worldwide)

and available-to-promise

inventory

(ATPI) order line

check, still could

not have been

sufficient to

comprise a holistic

SCM strategy.

Scala

Connectivity Solutions,

which are already

deployed in over

100 sites in over

thirty countries,

provide interconnectivity

to any best-of-breed

products (e.g.,

CRM, SCM, e-commerce

site integration,

warehouse

management system

[WMS], bar code

for distribution,

SAP, or personal

digital assistant

[PDA]-based module

solutions) would

likely not have

sufficed for the

target market’s

one-stop-shop

requirements.

Therefore, iScala

presents an opportunity

for third party

specialists or

VARs to create

add-on modules

providing functionality

geared to a targeted

market and meet

the specific needs

of a group of

users. Not to

mention that many

ready-made solutions

from the Epicor’s

arsenal (e.g.,

SRM, PLM, WMS,

storefront commerce,

etc.) could come

in handy for potential

up-sell and cross-sell

purposes.

Hence,

in addition to

a number of potential

functional extensions,

Scala finds a

more visible ‘big

brother’

with a global

infrastructure

(i.e., Epicor

generated nearly

$150 million (USD)

in revenue in

fiscal 2003, which

should still rank

it amongst the

dozen or so largest

enterprise applications

vendors in the

world) and a solid

management team,

more certain R&D

budgets, while

both companies

should jointly

garner increased

visibility and

clout. Both user

communities should

benefit from Epicor’s

enlarged size

(a substantial

installed base

of over 20,000

customers), and

recently restored

financial stability

and likely mutual

products’

enhancements (e.g.,

Epicor could leverage

Scala’s

HR and payroll

modules or localization

capabilities,

rather than typically

licensing them

in an original

equipment manufacturer

[OEM] fashion).

Epicor

Contribution

On

the other hand,

Epicor has embraced

.NET even more

zealously than

its creator Microsoft,

often leaving

Microsoft staffers

in their development

labs with their

dropped jaws.

As a good example,

over two years

ago, the vendor

released Clientele

CRM .NET

as a pure .NET-based

product (see Epicor

Claims the Forefront

of CRM.NET-ification).

Further, at the

company level,

Epicor’s

standardized technology

direction currently

embraces the Microsoft

.NET Platform

for XML-based

Web services.

Through .NET,

which is the next

generation of

Microsoft's

Distributed interNet

Applications Architecture

(DNA)

and Component

Object Model

(COM),

the vendor hopes

to be able to

provide comprehensive

support for Web

services deployment

and enterprise

application integration

(EAI).

This

technology strategy

should enable

Epicor's still

diverse development

teams to leverage

Microsoft technology,

while allowing

each product group

to continue using

the individual

databases and

development tools

appropriate to

the requirements

of each product's

target market.

For example, with

the release 6.0

of both the Vantage

and Vista

manufacturing

products early

in 2003, Epicor

executed on a

critical milestone

of its manufacturing

product roadmap—incorporating

a single application

framework across

the two solutions

through the alliance

with Progress

Software Corporation,

as well as with

Sonic

Software Corporation

for its enterprise

service bus for

transactions services

and security.

Furthermore,

in late 2004,

Epicor will introduce

its .NET-based

Vantage

8.0 manufacturing

solution (formerly

code named Project

Sonoma),

which features

an n-tier architecture

that has been

architected from

the ground up

to support the

.NET platform

and Web services.

Rather than wrapping

existing applications

with Web service-like

interfaces, the

new Vantage and

Vista presentation

layer has completely

been rewritten

in C# and Visual

Studio.NET,

while the extensive

business logic

has been preserved

and wrapped around

with stateless

Web services (i.e.,

which are connected

or invoked only

when the information

is needed).

The

platform will

supposedly deliver

unrivalled flexibility

and performance

for both developers

and customers,

and allow for

the development

of applications

based on Web services

that have either

a smart client

or browser-based

UI. Version 8.0

will include frameworks

for exposing all

applications interfaces

as Web services,

plus an orchestration

engine for constructing

composite applications

using both Microsoft

BizTalk Server

and Sonic.

The solution aims

at enabling all

(both existing

and future) Epicor

manufacturing

customers to adopt

Web services piecemeal,

on their own time

frame, while protecting

the existing technology

investment, since

software reuse

and integration

have been on Epicor’s

mind during the

software revamp.

Also

at the corporate

level, the vendor

has incorporated

numerous features

into its UIs to

simplify the operation

of and access

to all its products,

which incorporate

the popular Microsoft

Windows

graphical

user interface

(GUI). Epicor’s

GUI tools include

industry-standard

field controls,

pull-down menus,

tool bars, and

tab menus that

facilitate the

use of the software,

while the products

incorporate the

latest and most

advanced GUI features

such as process

wizards, cue cards,

advanced on-line

help, and on-line

documentation,

based upon today’s

single document

interface

(SDI) standards.

As the model for

distributed computing

continues to evolve

through the advent

of Internet technologies,

Epicor also offers

additional client

deployment models,

including thin-client,

browser-based,

and mobile client

access.

Therefore,

Epicor has lately

created three

diverse and yet

streamlined product

lines (i.e., Epicor

Vantage,

Epicor

iScala,

and Epicor

Enterprise)

that cover different

industries (i.e.,

distribution,

industrial, manufacturing,

services, non

profit, and hospitality

verticals) with

a minimal overlap,

which should mean

more opportunities

without much clash

amongst different

sales forces.

Epicor is striving

to become a cross-trained,

functional organization,

given some cross-selling

opportunities

in hospitality,

as well as localization

of manufacturing

with Scala accounting

and payroll solutions.

However, the other

side of the coin

is that because

of these seemingly

unrelated product

lines, Epicor

may mean different

things to different

people, which

does not really

help mind share

creation in particular

segments of interest.

Epicor,

as well as its

product groups,

have had a share

of tough history

that they now

must get far beyond

to gain traction

in the market.

For example, first

DCD,

then DataWorks,

and then Epicor’s

Manufacturing

Solutions Group,

the reborn manufacturing

group must remind

its customers

and the marketplace

of its historic

success and forget

about so many

years of financial

pressures which

nearly sunk it

into oblivion.

There would be

an analogy with

the Epicor

Enterprise Solutions

group, that started

as Platinum,

and has meanwhile

been awkwardly

and confusingly

till recently

referred to as

the “e

by Epicor”

umbrella brand.

Consequently,

since the late

90’s Epicor’s

business has been

less visible to

the market, and

customers and

the marketplace

may have forgotten

who Epicor Manufacturing

or Epicor Enterprise

are and what they

represent. The

positive industry

coverage for the

last two years

for its plausible

strategy, modern

products, and

record performance

are certainly

a great step in

the right direction.

Challenges

Despite

notable functional

and technological

initiatives, the

challenge for

Epicor/Scala and

its affiliate

channel also remains

the management

of still multiple

ERP product lines,

given iScala fits

somewhere between

the manufacturing

and service industries.

Also, while these

three major product

lines may have

their separate

niches, they will

in many instances

be similar enough

to confuse former

separate Epicor

and Scala’s

direct sales reps

and VARs in selling

the combined portfolio,

although Epicor

has defined specific

“rules of

engagement”

around functionality

and multinational

requirements.

Again coming back

to the brand management

conundrum, while

there is the intention

to drop the Scala

name in favor

of Epicor globally,

in many markets,

however, the Scala

name has much

greater specific

weight than Epicor,

which has led

the vendor to

keep the Epicor

Scala brand in

these regions..

The

management team

will further have

to determine a

narrow range of

key go-to-markets

for each product,

clarify the positioning,

and segment and

target the sales

channels. Although

it is likely that

the product lines

will continue

on their separate

tracks for some

time to come,

the newly combined

company should

unequivocally

articulate any

plans on future

product development

and possible cross-integrations.

To that end, while

there have been

many knee-jerk

temptations to,

for example, leverage

iScala’s

HR/Payroll and

localization capabilities

(tailored for

local language,

tax, and legislative

requirements)

for Epicor Vantage

or to integrate

the Epicor

for Service Enterprises

product to iScala

(and thereby create

more global opportunities

in both instances),

there have not

been many firm

decisions yet.

Till then, it

is still likely

that the sales

channel will face

some conflict

in terms of market

overlaps (e.g.,

the hospitality

vertical), as

well as traditional

association with

a certain product

line regardless

whether it is

the best fit for

a certain opportunity

(i.e., iScala

for global hotel

companies and

where the property

management is

critical versus

Epicor

Enterprise for

Hospitality

where the food

and beverage services

capability is

of more importance).

Moreover,

limited financial

resources to adequately

fund multiple

key strategic

initiatives including

multiple products’

assimilation,

brand marketing,

undeveloped global

channel and brand

recognition, and

formidable competition

within the market

of Epicor are

the challenges

the company has

yet to overcome.

Although Epicor

has a demonstrated

two-year track

record that shows

it has been able

to achieve profitability,

while continuing

to support all

of its products

with new releases,

and while delivering

new technology-based

products to the

market, if one

wants to be nit-picking,

the envisioned

annual revenues

of $250 million

(USD) for the

merged entity

is still less

than the revenues

of Epicor alone

back in 1999,

when it recorded

total revenues

of $258 million

(USD).

One

can also be nit-picking

when it comes

to the technical

foundation of

the three product

lines. Namely,

despite the Microsoft-centric

nature of the

products, with

many common denominators,

these products

are still not

on the same architectures.

To be more precise,

Epicor for Service

Enterprises is

built with the

Epicor

Internet Component

Environment

(ICE),

a new toolset

(created using

Microsoft Visual

Studio.NET and

the .NET Framework)

for the swift

development of

enterprise-class

Web services applications

and the foundation

for the new breed

of industry-specific

ERP solutions

from Epicor.

Within

the same product

breed, the Clientele

CRM.NET

suite, which was

the first CRM

application built

completely on

Microsoft’s

.NET Platform,

also uses Microsoft

Visual Studio

.NET as its standard

customization

tool and can support

changes using

any of the NET-compatible

programming languages,

but it uses rich

or smart client

versus Epicor

for Service Enterprises’

Web-based UI.

There are some

thoughts about

coalescing these

products’

architectures

into one in the

future (given

only nuances in

their architectural

differences),

but the greater

problem might

lie in the fact

that earlier Clientele

versions and other

Epicor Enterprise

industry-specific

products are quite

behind when it

comes to their

migration from

client/server

(i.e.,

Microsoft Visual

basic for Applications

[VBA]-based)

architectures

to Web service-based

one of, for example,

Epicor for Service

Enterprises.

More

Challenges

Epicor

Software Corporation

(NASDAQ: EPIC)

and Scala

Business Solutions

(formerly Euronext:

A.SCALA), an Amsterdam,

the Netherlands-based

provider of collaborative

enterprise software

for mid-size enterprises

and subsidiaries

of global corporations,

have completed

a merger that

began in late

2003. The merger

creates the largest

independent global

mid-market provider

of collaborative

ERP, customer

relationship management

(CRM), and supply

chain management

(SCM) applications

based on Microsoft’s

.NET

platform and Web

services, with

approximately

$250 million (USD)

annual revenues,

nearly 1,500 employees,

and with over

20,000 customers.

The combined company

hopes to expand

its global presence

with worldwide

coverage of sales,

consulting, and

support for mid-market

and large multinationals

as well as local

enterprises, offering

a broad suite

of integrated

solutions.

The

situation may

become even more

complex in Epicor’s

Manufacturing

Solutions Group,

which contains

6,500 of Epicor’s

20,000 customer

base, and which,

as mentioned earlier

on, features Vantage

(for new business

opportunities),

Manage

2000,

and Avant�

as its major mid-market

ERP products and

Vista

for smaller discrete

manufacturers.

As for specialization,

Vantage remains

the preferred

system for MTO,

job shop enterprises,

while Avant�,

which has not

been actively

marketed in the

U.S. since 1999,

leans towards

complex manufacturing

and project work

environments as

well as towards

repetitive manufacturing

with one of its

product variants;

Vista, on its

hand, is the low-end

product for much

smaller discrete

manufacturing

enterprises.

However,

even with this

simplified product

set, Epicor still

has a substantial

rationalization

and abridging

job to do. For

example, the vendor

has to utilize

open database

technology to

provide flexible,

yet integrated

enterprise business

applications.

Namely, Vantage

and Vista, developed

on a single framework,

are designed for

Progress Software

Corporation's

Progress

RDBMS,

but they are also

available on the

Microsoft

SQL Server .NET

Enterprise Server

platform,

while the Avant�

product leverages

UniData

(a.k.a. U2)

open database

technology from

IBM Corporation.

Thus,

the above-described

product roadmap

strategy within

Vantage 8.0 calls

for a common platform

that has a single

layer of business

logic and multiple

UIs that sit on

top, letting manufacturers

migrate from their

current installations

at their comfortable

pace. Epicor first

delivered on the

new roadmap with

the early 2003

announcements

that its Vista

6.0 and

Vantage

6.0 enterprise

systems now share

that common platform,

with UIs and workflows

tailored to the

markets they serve

(see Epicor

Reaches Better

Vista From This

Vantage Point).

At the same time,

Epicor rolled

out the product

strategy and roadmap

to all of its

manufacturing

customers, thereby

sharing the vision

of how all products

(Avant�, DataFlo,

Manage 2000, and

ManFact) would

fit into the future

constellation,

including plans

to continue development

on those solutions

releasing new

upgrades every

12 to 18 months

based on customer

feedback. Logically,

Vantage and Vista

have taken the

front seat as

the solutions

for new business,

owing to their

sexier technological

foundation.

While

the long awaited

porting of Epicor’s

flagship products

onto Microsoft

SQL Server and

Progress as well

as continued focus

on .NET framework

should significantly

relieve the company's

R&D burden

(the vendor spends

12 percent of

its revenues on

R&D, and has

over a quarter

of its total headcount

in R&D), create

incremental revenues

opportunity in

coming years and

improve its general

competitiveness,

the remaining

work of delivering

single .NET compliant

application framework

remains major.

At best, 80 percent

of current install

base will be covered

by the first release

of Vantage 8.0—namely,

the earlier users

of Vantage and

Vista, whose migration

(or mere “cherry

picking”

of new Web service-based

enhancement) should

be reasonably

painless.

Eventual

Migration

Still,

the remaining

20 percent of

6,500 manufacturing

customers, might

sooner or later

want to migrate

from current non-.NET

applications,

although Epicor

is committed to

supporting these

customers indefinitely

(these customers

are currently

provided with

new upgrades every

12 to 18 months

based on the input

the vendor gets

from customers

with regard to

the enhancements

they would like

to see), which

will in turn draw

on its multiplied

R&D and support

resources. One

should imagine

the magnitude

of the effort

when the Avant�

and Manage 2000

(Epicor acquired

ROI Systems in

mid-2003, bringing

this midsize discrete

manufacturer and

hybrid manufacturing

and distribution

environment enterprise

solution to the

fold) instances,

some with extensive

customer bases

on non-Microsoft

technologies,

should follow

the path. Epicor

indicates that

these customers

will be offered

a migration to

Progress or IBM

DB2 database

from U2 (only

in the second

generation of

Vantage/Sonoma),

but acknowledges

that the migration

will virtually

be another full-fledged

implementation,

which might mean

some customers’

defections.

As

for Scala, room

for functional

enhancements beyond

ERP and product

delivery work

in progress remains

too. Namely, despite

the elaborately

thought out transition

between the products

(the upgrade path

from Scala

5.1 to

iScala

2.2 is

reportedly no

more complex than

that between service

releases of Scala

5.1), Scala does

not intend to

immediately withdraw

Scala 5.1, as

there are still

existing customers

who are in the

middle of a roll

out of the product

and as not all

languages have

been implemented

in the initial

releases of iScala.

Further,

the company has

to build the hospitality

and pharmaceutical

functionality

into a forthcoming

new release of

iScala 2.2. The

partnership with

Microsoft

for CRM

might also be

dubious in the

long run, given

the temptation

to utilize the

‘home’

product Clientele,

particularly for

some larger enterprises

where Microsoft

CRM scalability

is yet to be tried

and true.

Competition

Incidentally,

the competition

is also flying

from many directions

since the parent

company now competes

in many diverse

markets, and it

now has a number

of competitors

that vary in size,

target markets,

and overall product

scope. The primary

competition comes

from ISVs in three

distinct groups,

including

1)

The above-mentioned

large, multinational

tier one ERP

vendors that

are increasingly

targeting midsize

businesses as

their traditional

market becomes

saturated (see

PeopleSoft

Revamps World

for Its Mid-Market

"Express" Conquest

and SoftBrands

to Institute

Fourth Shift

for SAP

Business One

Manufacturing

Work-Plan).

2) Midrange

ERP vendors,

including Lawson

Software,

SSA

Global,

IFS,

Intentia,

and MBS.

3) Established

best-of-breed

or point solution

providers that

compete with

only one portion

of Epicor’s

overall ERP

suite, including

Sage/Best

Software,

Systems

Union,

Unit

4 Agresso,

or Geac

for financial

accounting;

HighJump

Software,

Prophet21,

RedPrairie,

or Manhattan

Associates

for distribution

and

WMS;

QAD,

MAPICS,

SYSPRO,

Lilly

Software,

Encompix,

Adonix,

or Made2Manage

for manufacturing;

and Onyx,

Siebel

Systems,

Pivotal,

FrontRange,

Salesforce.com,

or SalesLogix

(owned by Best

Software) for

sales force

automation

(SFA), customer

service, and

support. The

list of the

competitors

in the above

markets is by

no means exhaustive.

Also,

a leaner company

with a large customer

base and a palatable

market capitalization

remains an attractive

acquisition target

in this seismically

consolidating

market, with possibly

unwanted attention

of predatory competitors.

At least, the

Scala acquisition

with its organizational

and products’

merger might also

deter the acquisition-spotting

vultures for the

time being, in

addition to an

existing rights

plan for a heftily

higher price per

share than the

current one.

User

Recommendations

Epicor’s

financial stability

and its ability

to enhance its

products (both

in-house and via

acquisitions)

and its determination

on executing product

and technology

strategies deserve

commendation.

Current users

are advised to

follow Epicor's

new product introductions

and keep an eye

on its future

product strategy.

The positive sign

is the company’s

more manageable

and narrower focus,

as demonstrated

by its most recent

results. Mid-market

companies with

up to $1 billion

(USD) in revenues

that are within

the parent Epicor’s

industries of

focus (i.e., Epicor

Vantage

for capital equipment,

fabricated metals,

electronics, instruments

and controls,

and consumer

packaged goods

[CPG], and Epicor

Enterprise for

enterprise services,

financial services,

non-profit, hospitality,